04 Aug 2025

DAX Index Technical & Market Analysis

The DAX index experienced a sharp decline of 2.66% on August 1 amid rising US stagflation concerns and weaker-than-expected China PMI data. This selloff reflected growing worries over a global economic slowdown, with auto and banking sectors leading the losses.

Market Overview

DAX closed at 23,426 after back-to-back drops, weighed down by fears of weakening demand and geopolitical tensions. Auto stocks such as Daimler Truck (-8.71%) and Volkswagen (-3.21%) suffered significant declines amid uncertainty around global growth.

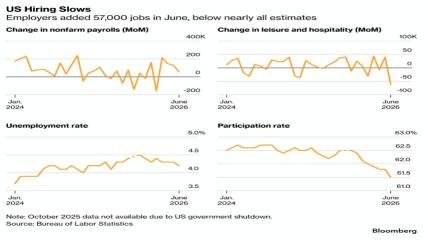

US labor market data added to market jitters as July’s jobs report revealed slower payroll growth and rising unemployment, fueling stagflation fears. This led to broader risk aversion, impacting both European and US equities.

Technical Outlook

From a technical perspective, the DAX is currently trading below its 50-day EMA but remains above the 200-day EMA, signaling bearish momentum in the short term but a potentially bullish longer-term trend.

Upside Potential: A break above the 50-day EMA near 24,000 could pave the way for a rally toward the July 10 record high of 24,639.

Downside Risks: A break below key support at 23,350 may lead to a test of the 23,000 level and further downside pressure.

The 14-day RSI stands at 38.41, suggesting there is room for further downside before the index enters oversold territory.

Market Drivers

Looking ahead, the DAX’s direction will largely depend on upcoming US Services PMI data and central bank communications, particularly from the Fed and ECB. Positive economic data and dovish central bank rhetoric could boost sentiment and support a recovery. Conversely, weak data or hawkish policy signals could pressure the index lower.

Conclusion

Traders and investors should closely monitor key economic releases and central bank guidance to navigate the current volatility. While expectations of a Fed rate cut are providing some optimism, risks related to stagflation and slowing global growth remain significant.

Latest Posts